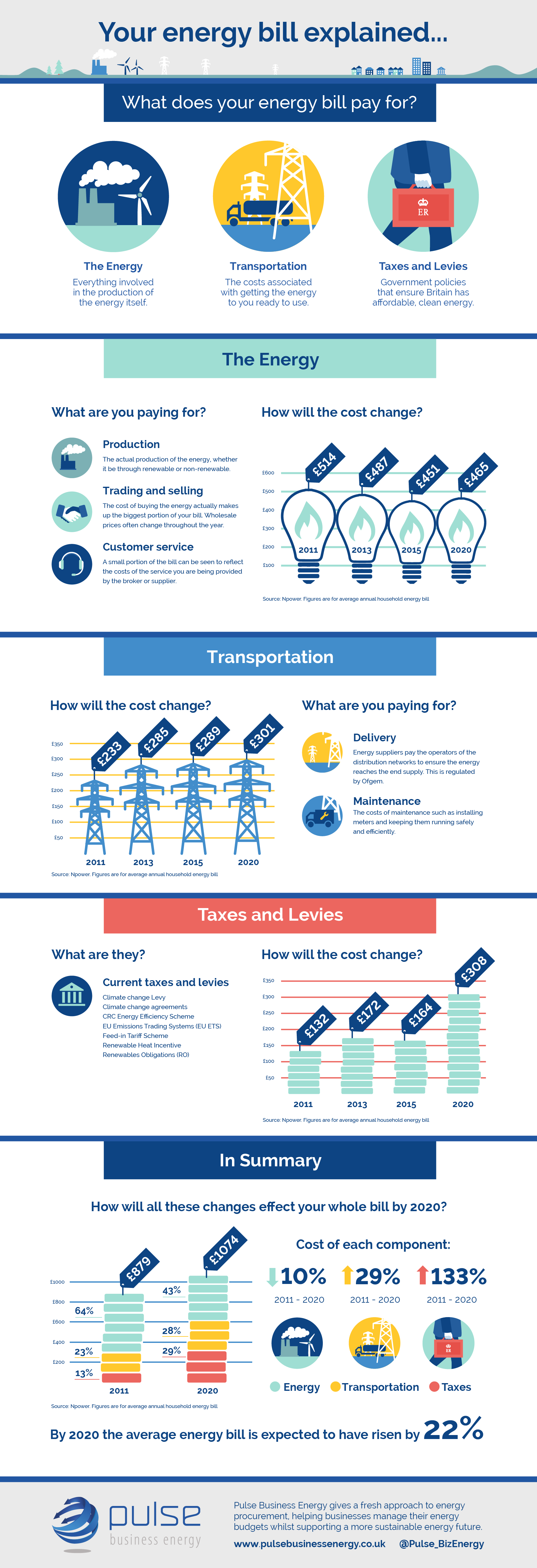

The global energy map just got a lot smaller, and if you’re sitting in Tokyo, Seoul, or Taipei, it’s looking incredibly crowded. We’ve spent years talking about "energy transitions" and "diversification," but the reality of 2026 is much grittier. When a missile hits a gas processing plant in the Middle East, the lights don't just flicker in Tehran. They start to dim across the Pacific. The current escalation involving Iran and the strikes on critical gas infrastructure isn't just a local skirmish. It's a direct hit to the heart of Asian industrial stability.

Asia is the world's largest importer of liquefied natural gas (LNG). Countries like Japan and South Korea have almost zero domestic resources. They rely on a steady, unbroken chain of tankers moving through the Strait of Hormuz and the Malacca Strait. When Iranian gas fields or regional export hubs become targets, that chain doesn't just stretch—it snaps. We aren't just looking at higher prices at the pump. We're looking at a systemic threat to the manufacturing hubs that power the global economy. Meanwhile, you can explore other events here: The Cold Truth About Russias Crumbling Power Grid.

The Fragility of the LNG Bridge

Natural gas was supposed to be the "bridge fuel." It was the cleaner alternative to coal that would carry Asia toward a green future. But that bridge is built on some of the most volatile geography on Earth. The recent strikes on Iranian gas infrastructure have sent a clear message: the energy supply is now a primary target, not just collateral damage.

Iran holds some of the world’s largest gas reserves, specifically the South Pars field. While Iran isn't a massive exporter of LNG to Asia compared to Qatar, its role in the regional grid is massive. When Iranian production drops or its infrastructure is crippled, the entire Middle Eastern energy balance shifts. Qatar, the neighboring giant, shares the same geological structures. If the conflict spills over or if shipping lanes are choked, the "bridge" collapses. To explore the full picture, we recommend the excellent article by The Washington Post.

You have to understand the math here. Japan and South Korea together account for nearly 40% of global LNG imports. They don't have pipelines. They have ships. If those ships can't move because of regional instability or if the gas they’re supposed to carry isn't being pumped, there’s no Plan B. Batteries aren't ready to scale yet. Coal is being phased out. The desperation is real.

Why the Iran Conflict Hits Asia Harder Than the West

Europe spent the last few years frantically decoupling from Russian gas. They built floating terminals and locked in contracts. They’re tired but somewhat stabilized. Asia, however, didn't have the same "wake-up call" until now. Much of the Asian energy strategy relied on the assumption that the Middle East would remain a stable, albeit tense, gas station.

When strikes hit gas fields, the immediate effect is a "risk premium" on every British Thermal Unit (BTU) sold on the spot market. But the long-term effect is worse. It’s the death of predictability. Manufacturers in Taiwan or Vietnam operate on razor-thin margins. A 30% spike in energy costs—driven by a war halfway across the world—can make an entire semiconductor plant or textile factory unprofitable overnight.

I’ve talked to analysts who say we’re seeing a "permanent war footing" in energy pricing. It means the days of cheap, reliable gas are likely over. We’re entering an era where the cost of energy includes the cost of a private navy or the massive insurance premiums required to sail through a combat zone.

The Domino Effect on Global Supply Chains

It’s easy to think of this as just a "gas problem." It’s not. It’s a "everything problem."

Consider the production of fertilizers. Natural gas is the primary feedstock for nitrogen-based fertilizers. If Asian countries have to pay double for gas to keep their cities lit, they’ll stop making fertilizer. This leads to lower crop yields across Southeast Asia. Now you have an energy crisis turning into a food security crisis.

- Manufacturing slowdowns: Factories in China and India that rely on gas-fired power will face rolling blackouts.

- Inflationary pressure: Everything from electronics to car parts gets more expensive because the energy used to build them costs more.

- Currency devaluation: When countries have to spend more of their foreign reserves to buy expensive energy, their local currencies take a hit.

The interconnectedness is staggering. A drone strike on a processing plant in the Persian Gulf can be directly linked to a price hike for a smartphone in New York or a bag of rice in Manila.

What Most People Get Wrong About Energy Security

There's this common myth that "renewables will solve this." I wish it were that simple. Solar and wind are great, but they don't provide the high-heat baseload power needed for heavy industry. Not yet. In the short term—the next five to ten years—Asia is stuck with gas.

Another misconception is that the U.S. can just "export more" to save the day. The U.S. is already pushing its export limits. There are only so many LNG terminals and only so many tankers. Plus, the U.S. has its own domestic political pressures to keep gas prices low for American voters. Relying on the U.S. as a "white knight" is a dangerous gamble for Asian leaders.

Moving Toward a New Energy Reality

Asian governments are finally reacting, but it's a slow-motion pivot. We're seeing a massive reinvestment in nuclear power in Japan and South Korea. It’s controversial, sure, but when the alternative is economic collapse, "controversial" starts looking like "necessary."

Countries are also looking at "friend-shoring" their energy. They’re trying to sign 20-year deals with stable partners like Australia and Canada. The problem? Everyone else is trying to do the same thing. The competition for "safe" gas is becoming a bidding war that the developing nations in Asia might lose.

You should expect to see a lot more "energy nationalism." Countries will start hoarding supplies. They’ll prioritize their own domestic industries over exports. This "me-first" approach will only make the global market more volatile.

Practical Steps for the Road Ahead

If you’re running a business or managing investments that depend on Asian markets, you can't afford to ignore the geopolitical reality of gas.

Start by auditing your energy exposure. If your supply chain relies on factories in regions heavily dependent on imported LNG, you need a backup plan. This might mean diversifying your manufacturing footprint to countries with more domestic energy stability, like Indonesia or parts of the Americas.

Invest in efficiency now. It sounds like a cliché, but it's the only immediate defense against rising costs. Every watt saved is a watt you don't have to buy at a war-premium price. Companies that can operate with 20% less energy will be the ones that survive the next decade.

Keep a close eye on the "insurance" side of shipping. If the Middle East remains a hot zone, the cost of moving goods through the Indian Ocean will continue to climb. Factor these "hidden" costs into your long-term contracts today. Don't wait for the next headline about a gas field strike to realize your margins have evaporated.